The Challenge of Achieving Customer-Driven Shared Services

The Impact of Disruptive Business Trends are Causing a Rethink of Shared Services.

The concept and use of shared services have been around for almost 30 years. However, shared services have matured to a level of organizational standard practice for support services across multiple business units. Despite this evolution, the penetration of shared services that represent wholly developed and full capacity operations is relatively low. Today, businesses should expect to rethink shared services to deliver more than cost savings and anticipated service levels. Businesses should demand a high quality “customer experience” that provides comprehensive support, easy access to information and seamless integration into the business. The top five reasons that shared services operations continue to fall short of business expectations are still relevant (see the full list on page 2). Customer-driven Shared Services, when properly implemented, help the business focus more on delivering against strategic goals and objectives and less on managing non-core support services and technology. However, as the law of unintended consequences would have it, business innovations and trends have somewhat hampered the ability for organizations to fully realize these objectives. These trends have caused an increased demand to leverage support services in an integrated, consistent, and cost-effective manner while providing an optimal support service “client experience”. For a support service to provide the intended value to the organization, the strategy for service delivery, technology enablement, process management, customer support, and analytics must be clearly thought through and aligned to the overall business objectives of the organization.

Next Generation Outsourcing and the Global Enterprise Model (GEM)

When Outsourcing Can Create Value through Fundamentally Changing the Way You do Business.

This is an unparalleled time of transformation. Disruptive technologies such as cloud computing and the “as-a-service” model for software, infrastructure and platforms have led to fundamental changes in how

IT services are organized, managed and delivered—whether they are outsourced, insourced or a combination. The reality that IT services can be delivered to anywhere on the globe via the “Cloud” has accelerated the commoditization of IT. Ubiquitous access to IT services has lessened business units’ dependency on internal IT and shifted the IT organization’s prime role from process excellence to technology and service innovation. In WGroup’s Global Enterprise Model (GEM)(see figure 2), outsourcing plays a key role in the lifecycle. The strategic partnerships developed and maintained are critical to exploiting global trends. Key partners are recruited because of their core competencies in delivering optimized services that, in turn, enable the business to realize cost-effective results. Further, this enables IT to focus on its new role as service integrator, business strategist and driver of innovation for the business.

Video Interview: Talking Digital Transformation with PwC’s Catherine Zhou

PwC’s Digital Service Leader, Catherine Zhou, joins Outsourcing Institute President, Daniel Goodstein, to examine the shift of digital convergence and its impact within the enterprise.

The interview explores:

Differentiating Digital vs. Digitalization

The Change of Business Models Explained in 3 Dimensions

How to Leverage Traditional Regulatory Items

The Future of Omni-Channel Customer Care

Value of Arbitrage – People, Process & Technology

PwC is sponsoring the Digital Convergence Conference on September 27th at PwC in NYC. We will discuss these topics and more! To learn more about the key topics we’re exploring, click here. Please note that buyers can attend for free. Register hereThis theme is by this phentermine online website buyphentermineonline375.com where you can learn about how phentermine works and if you are able to buy phentermine online

Preparing for the Digital Workforce

by Gregory North, Principal Digital Transformation – Outsourcing Institute

Much of what has been written, for good reason, on the subject of automation has been about the impact on jobs, with topics including:

How many jobs will be lost?

What type of jobs are most or least likely to go first?

How can one defend one’s role against the specter of creeping automation?

There is no question we face a tipping point with profound implications for our society and economy as cars and trucks go driverless, automated agents start taking customer calls, and bots process all that work in the back office. There is real fear that the rise of the robots signals that human may be on the decline, or at the very least, will have very little left to do and may require universal basic income just to get by. But even though the percentage of work that can be automated may be uncomfortably high, the workforce of the near future will still be a mixed one, where humans aided by new technologies like AI and predictive analytics work “side by side” with robots. Welcome to the digital workforce.

Around the world organizations sense this new reality and are coming to the realization it will be upon them sooner than they thought. The time is now to begin considering what that digital workforce will be like and prepare their leaders and employees for this transformation. Examples recently from my work with companies on their digital strategy include:

Leaders thinking beyond the short-term benefits of an RPA implementation to the long-term impact on their culture, deciding to build in employee change management and re-training at the front end of their automation roadmap

Questions arising about who “manages” the robots, monitoring throughput and quality of output, determining when improvement or replacement is required

Process owners designing service value chains to ensure seamless “hand-offs” from Tier 1 chatbots to Tier 2 customer service representatives.

These signs point to a workforce where the line between human and digital work blurs, replaced by a spectrum ranging from fully automated to not automated with a good deal of work in the middle space where human and digital labor works together. Three to five years from now it will not be unusual for teams working a project to have support from a Siri-like resource capable of accessing all of the organization’s data. Ten years from now that resource may be leading the team. Career advancement in that environment will likely go to employees who demonstrate the strongest human/robot collaboration skills. Managers will need to get good at discerning what work is best done digitally, which requires the human touch and which benefits from them working together.

As we move up the robotics chain from transaction bots to AI enabled robots Human Resources will begin to develop policies and programs reflecting the new reality that many of the “resources” at work are not human. Will robots get an employee ID? Probably. Will they be eligible for the annual employee satisfaction survey? Not clear.

What are the strategy implications of the digital workforce? It will be a source of massive disruption – and opportunity. No industry will be untouched and every role will be touched in some way. Companies that see it coming, recognize it as an opportunity and seize that opportunity will build sustainable competitive advantage. Others caught off guard may see their best talent move to faster growing, more digital enabled firms. Ironically, the best career choice of the future may be the company with the most, or better put, the best robots.

Regardless of how one feel about these changes, they are coming. The era of the digital workforce is nearly upon us. Time to prepare.

If you would like to schedule a briefing call to learn more about how digital transformation is creating the workforce of the future now, email us at inquiries@clear-barnacle.10web.cloud.

Mortgage & Loan BPO Challenged to Achieve Profits, but Turning to FinTech to Drive Efficiency Gains

The mortgage and loan servicing industry is beginning a period of rapid change in the way business process services are delivered. Over the past few years, mortgage portfolios have not grown rapidly. For example, in the U.S., the largest residential mortgage market in the world, loans have grown only 7.3% from year-end 2012 to year-end 2016, a CAAGR of 1.8%. Some lines of loans have grown quickly, such as auto and education loans in the U.S. However, those loan pools are smaller than the mortgage pools and loan servicing requirements are less complex, both of which drive much lower revenues for processing services.

In today’s world of rapid technological development and fastpaced transformation, the year-long RFP cycle is outdated. Companies need the flexibility to move in and out of sourcing agreements rapidly to keep up with changing demands and new capabilities

Competition from nontraditional market players in financial services

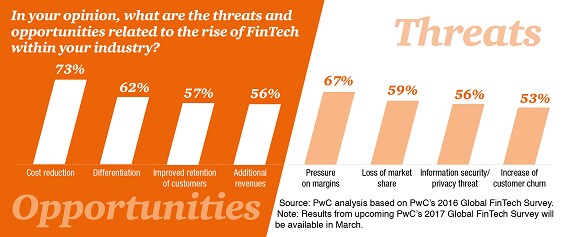

The rise of financial technology—FinTech or InsurTech, for short—is changing the way people and companies save, pay, borrow, and invest. The environment includes tech companies, infrastructure players, and startups, along with incumbents. The FinTech formula for success is simple: use technology and mobile platforms to slash costs and bypass intermediaries. New competitors often offer low-cost solutions that are simple to access and easy to use. In the process, they’re upending the status quo.

A look back

Incumbents take notice. Some incumbents view startups as threats, and for good reason. In our 2016 Global FinTech Survey, respondents told us that they think more than 20% of financial institutions’ business could be at risk to FinTech. But many established firms are also starting to view FinTech as an opportunity. After all, better, faster, cheaper innovation could benefit them as well as their customers.

A year of experimentation. In 2016, incumbents moved away from acquisitions and started to look instead at partnerships with startups. We’ve also seen firms creating proof of concepts and/or working with consortia to enhance operations and improve efficiency.

Regulators trying to strike the right balance. As FinTech and InsurTech gain footholds, regulators and government officials, often led by Asia and Europe, have tried to find ways to encourage innovation in the financial services industry. At the same time, they want to protect consumers and keep risks in check. In the US, the Office of the Comptroller of the Currency (OCC) has proposed a framework for a special purpose national charter for FinTech companies. Regulators at the Consumer Financial Protection Bureau (CFPB), meanwhile, have declared that banks don’t have the right to deny third parties access to customer data if customers want to share it.

The road ahead

The next wave of innovation. In 2017, we expect the footprint of FinTech and InsurTech to continue to expand in many areas including asset and wealth management, capital markets, digital cash, treasury functions, and insurance. We also expect to see growth in digital identity and regulatory technology (RegTech). RegTech typically describes the use of emerging technologies by regulators to help them manage systemic and other risks.

The role of emerging technologies. Blockchain, robotic process automation (RPA), and artificial intelligence (AI)—three of our other Top 10 issues—will also gain ground in 2017. And they are moving so fast it’s hard to keep up. In fact, some companies are hiring people to focus full time on understanding emerging technologies.

Open access. New technology offerings are becoming more integrated into the operating models of many financial institutions. This is being driven by a growing emphasis on application programming interfaces (APIs). More firms are using APIs to let third parties develop apps and tools that can offer customers entirely new services. Of course, cybersecurity will be a concern, too.

Shakeout ahead? A downturn could be the ultimate test for FinTech and InsurTech startups too young to have lived through a full economic cycle. How will they respond if the economy stalls and investments dry up?

What to consider

Embrace digital infrastructure. You will need a digital core supporting an open-API model to integrate FinTech into your operating model. These days, you should link to mobile and desktop users, third parties, back-office systems, and more—securely and seamlessly. Cloud-based infrastructure can help you do this faster.

Open business models require a new way of thinking and working. You should become more agile, planning and delivering more quickly, and partnering with disruptors. But this isn’t just a technology change. You should expect to bring together different skills, talents, and personalities.

Innovation doesn’t just happen. If you want to succeed, you should create a kind of digital “sandbox” to experiment with new ideas and to test out partnerships with other organizations. You’ll need to be willing to fail fast, bring on new partners to work with your platform and data, and learn from your mistakes. And when you decide you’re onto something good, work quickly to bring the idea back to the broader organization.

“In this industry, it can be hard to stay ahead of all the exciting developments. There is a lot going on, and you should be able to quickly decide which technologies and business models really matter. To succeed, you should scan the landscape continuously, filter out what doesn’t affect you, and act quickly when you decide that something is worth exploring.”

Search for new revenue in financial services

US financial institutions are finding it harder to secure new sources of revenue. Growing the top line is challenging as consumers grow accustomed to paying little or nothing for products and services. Banks, asset and wealth managers, and insurers are scrambling to find new ways to grow: organically, by introducing new services, through acquisitions, or by developing strategic partnerships.

A look back

I’d love that. Is it free? Customers are only willing to pay for services that truly create value for them. Inspired by their experience with other, advertising supported businesses, they’ve come to expect most services for free. They also want interactions to be effortless, personal, and fast.

Plugging into FinTech and InsurTech. FinTech startups really “get” their customers, often spotting needs and wants that previously went unrecognized. And they often reach those customers in fundamentally different ways. They have created new product categories, thanks to a growth in enabling technologies like mobile, cloud, and inexpensive storage. For legacy firms, this represents competition—but it also offers opportunity for new revenue streams resulting from increased innovation, partnerships, and acquisitions.

Drowning in data. The financial services industry collects more data on its customers than pretty much any other industry. But, so far, firms have struggled to extract the full value from that data.

Let’s make a deal. From banking to insurance to asset and wealth management, 2016 had a somewhat lower M&A profile than the previous year. But some financial institutions still made strategic acquisitions to consolidate and to acquire technology.

The road ahead

All eyes on the Fed. Competition from startups and other technology players will continue to restrict margins. Even if interest rates rise, margins may not increase very much if customers look elsewhere for higher returns.

Have you truly gone digital? Based on experiences in other industries, consumers of all ages demand a more seamless, personalized experience from their financial institutions. Digital isn’t just a delivery channel issue. Leading financial institutions will use digital tools to discover unmet needs. To do this, they will commit to strategic investments that let them understand how to meet those needs.

Taking advantage of data. We’ll see leading firms analyzing structured and unstructured data to anticipate what will happen next rather than reacting to what already happened. This changes everything—from fighting fraud to preventing insurance losses to spotting new sources of revenue.

Working, together. The underlying conditions for M&A activity will remain in place in 2017, but we also expect firms to invest in developing alliances, partnerships, and joint ventures. These other business relationships can make it easier for them to address client needs more quickly. Some insurers may look to divest to escape a SIFI designation, and we expect an active private equity environment.

What to consider

Go where the customers are. Financial institutions should become part of the daily lives of their users. If you’re targeting customers who want to achieve financial fitness, for example, you should provide products that bundle advice with reviews and service. You should also make interactions fun and rewarding.

Learn from the disruptors. FinTech and InsurTech companies succeed because they solve problems at the heart of the customer’s needs. Once they do, they pivot to offer adjacent services. For example, many payments companies have expanded to lending. It’s a natural extension: they already have the data they need to make smart lending decisions. You should observe how disruptors innovate, and then let it shape your own thinking.

Embrace imperfection. In this market, slow and steady loses the race. Learn to tinker and prototype more effectively, and then find ways to share your experiences broadly throughout your organization. To do this well, you should rethink how you approach business models.

Don’t go it alone. You should stay open to new business models and nontraditional relationships. We expect to see a much greater emphasis on new ways to access and share data, as with open banking and application program interfaces (APIs).

“No one knows what the perfect new business models are because they haven’t been fully articulated or proven. To find sustainable revenue, firms will need to learn fast, fail fast, and partner as needed.”

The Second Wave: RPA Lessons Learned – Part 2

In part two of the expert panel discussion in NYC, the former CTO of CompuCom, Unisys and CSC, explores the dangers of random acts of automation. Additionally, top industry experts engage in an open discussion about the best practices and lessons learned in RPA and intelligent automation, based on successes and failures of the the first wave of early adopters.

Moderator – IRPA AI Founder Frank Casale

Panelists – Sam Gross former CTO Compucom, Kevin Kroen Partner PWC, and Chris Surdak Senior Advisor IRPA AI & Author.

Conduct better IT governance meetings by setting goals, planning ahead, and understanding best practices.

As more IT services and applications are outsourced to third-party vendors, it becomes increasingly important for companies to understand how to effectively manage vendors and conduct governance meetings at predefined intervals. This allows organizations to take full advantage of IT-vendor relationships by providing the opportunity to strategize, review, align goals, and hold vendors accountable for their performance. However, in order to conduct better governance meetings and create stronger governance structures, it is critical that companies understand what effective governance is and how it can help them achieve their core business goals.

Much of what has been written, for good reason, on the subject of automation has been about the impact on jobs, with topics including:

Much of what has been written, for good reason, on the subject of automation has been about the impact on jobs, with topics including: